Cerebras disclosed everything. It framed almost nothing.

No investor deck, no fact sheet, no public-company narrative — just a 300-page S-1, three flattering headline numbers, and a share price putting the qualifiers back in frame. Researched with AI, judge

There’s no investor presentation to grade. No roadshow deck to read. No plain-English fact sheet. No public-company narrative. The investor-relations page is still a placeholder: investor events coming soon.

What there is, is a 300-page S-1. The key disclosures are in it. But the filing leaves the reader to assemble the story themselves.

That isn’t dishonesty. It’s a different kind of investor-communication problem.

When SpaceX went public, there was a story to inspect: the S-1, a fact sheet, the roadshow deck and a CFO-narrated video, all in one controlled place (spacexipo.com). You could disagree with the framing, but you could find it.

With Cerebras, the filing is the story. And when the filing leads with the flattering numbers, those numbers become the narrative by default. It’s why, asked to summarise Cerebras last week, an AI told me the company “turned profitable on revenue up 76%,” fluent, sourced, and wrong in the two places that decide whether either number is real. (The profit that wasn’t.)

Here’s the rule underneath all of it: a number means what it’s standing next to. A profit means one thing beside an operating profit and another beside an operating loss. Growth means one thing beside a broad customer base and another beside related-party concentration. A backlog means one thing from the open market and another from a customer who also bankrolls it. Cerebras disclosed every one of those qualifiers. It just didn’t put them in the frame. Three numbers show what that costs.

First, what’s on the table

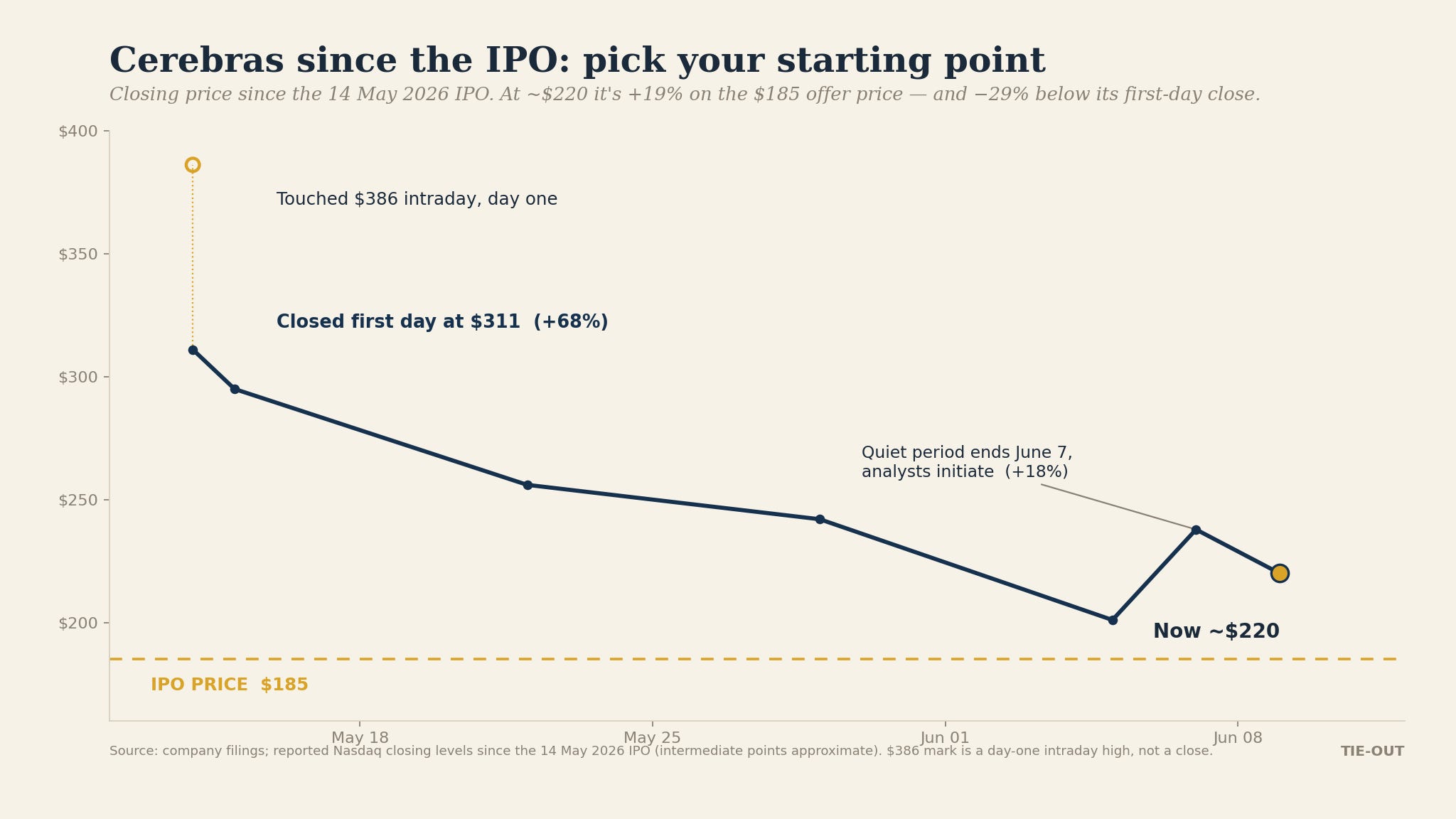

Cerebras priced its IPO on May 13 at $185 a share, above its marketed range, and raised about $5.55 billion — the largest US tech listing in years. It opened the next morning at $350, touched $386 intraday, and closed its first day up 68%.

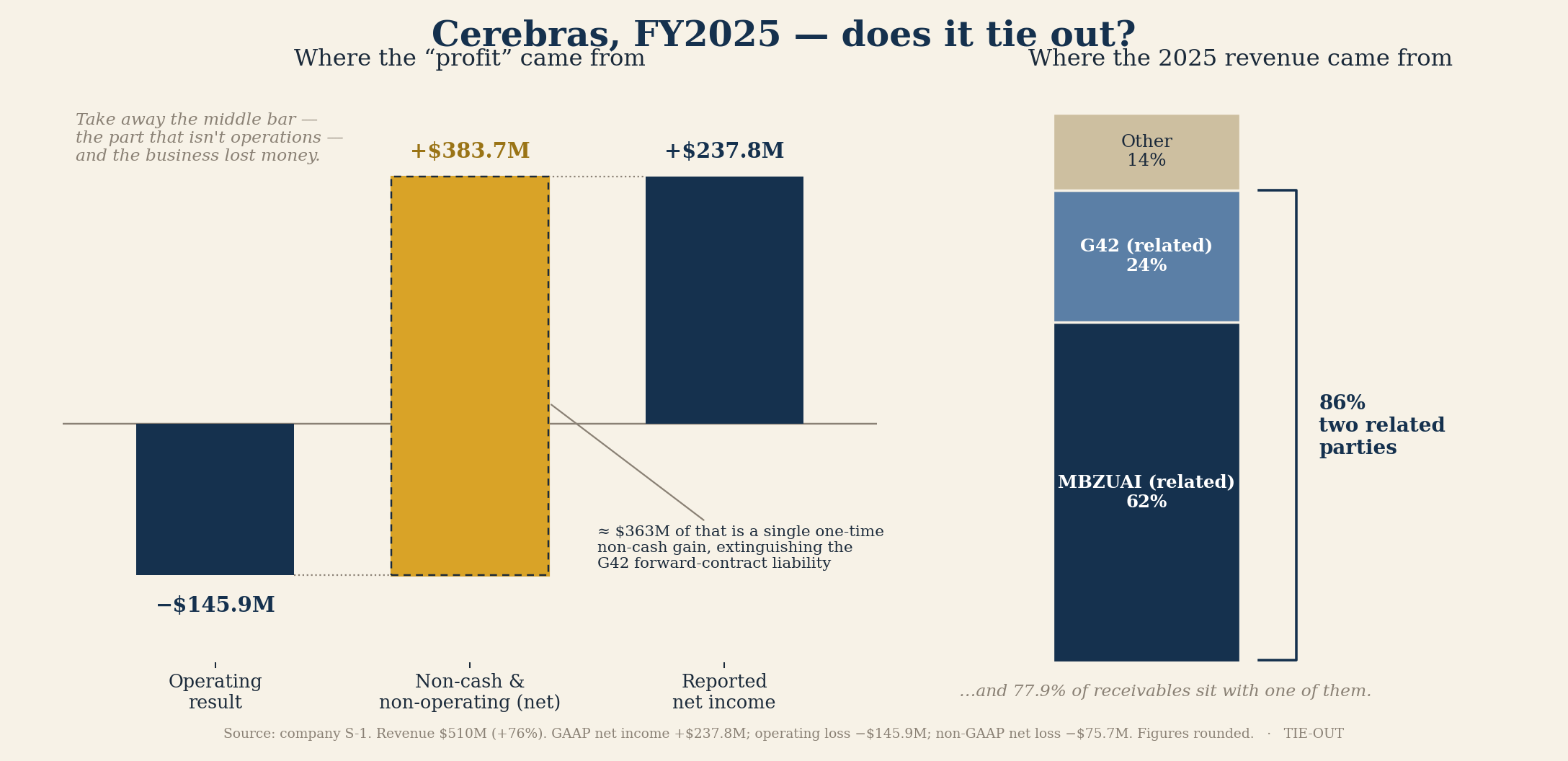

Then the numbers the listing was built on. FY2025 revenue was $510 million, up 76% (from $290.3 million); the bottom line was a $237.8 million GAAP profit; and the figure now doing the heavy lifting is a $24.6 billion backlog, roughly 48 times that revenue. A profit, a growth rate, a backlog. Take each one and look at what it was presented beside.

The profit, without the operating line

A $237.8 million GAAP profit reads as a company comfortably in the black — a swing from a $481.6 million net loss the year before. The operating business tells the opposite story: a $145.9 million operating loss, wider than 2024’s $101.4 million. The entire distance between the two is non-operating: chiefly a one-time, non-cash gain of about $363 million from extinguishing a forward-contract liability tied to G42’s original investment. It’s an accounting event, not a year of selling chips. Strip it out, as the company does in its own non-GAAP measure, and 2025 was a $75.7 million net loss.

None of that is concealed; it’s all on the income statement. But the presentation lets “net income, positive” stand on its own and a positive bottom line is what gets repeated, by an AI summariser, a headline, a reader in a hurry. What would tie it out is one line, in frame: operating result → the non-cash gain → net income. Shown together, fewer people mistake a liability revaluation for a business turning profitable. Shown apart, almost everyone does.

The growth, without the customer

“Revenue up 76%” reads like product-market fit. The qualifier sits in the notes: around 86% of 2025 sales came from two related UAE entities — MBZUAI at 62% and G42 at 24% — and one of them alone accounted for 77.9% of receivables. US-billed revenue actually shrank year-over-year. The prior year’s healthy-looking operating cash was largely a prepayment from that same group — the customer funding its own orders.

Growth and the source of growth belong in the same frame. “Grew 76%” and “86% from two related parties” aren’t two facts; they’re one fact told in halves. Put the growth rate beside revenue-by-relationship and you see what the number is: not a market forming, but a relationship deepening.

The backlog, without the counterparty

This is the one that matters most at today’s price, because it’s the $24.6 billion backlog, not the $510 million of revenue, that the valuation is leaning on. Framed simply as “backlog,” it reads as demand.

Read it next to its counterparty and it becomes a different asset. The majority of that backlog is tied to one customer: OpenAI, under a multi-year agreement for 750 megawatts of compute through 2028. And OpenAI is not an ordinary arm’s-length buyer: it is also advancing Cerebras roughly $1 billion and receiving warrants. That makes it a customer, a financier and a prospective owner.

A backlog from the open market and a backlog from a customer also bankrolling the supplier are not the same quality of asset. Only one of them tells you demand is truly independent. The disclosure says which one this is. The framing, “$24.6 billion backlog”, does not.

To be fair to the forward story: AWS and other channels may broaden the customer base. That’s exactly the development that would change this picture, if it shows up in the revenue rather than the narrative.

The CFO Rewrite

If I had twenty-four hours before this listing, this is the slide I’d insist on.

One slide, three panels, every qualifier in frame: the operating-to-net-income bridge; revenue by customer relationship; backlog by counterparty. Not a single new disclosure: everything on it is already in the S-1. Just the same numbers, set beside the things that decide what they mean. It costs the story its flattering reading, and that’s the point: a number presented with its qualifier in view is a number an investor can trust.

The Boardroom Test

Take an independent director’s seat and ask four questions:

Is the profit operating profit? No, a one-time non-cash gain sitting on a $146 million operating loss. Fail.

Is the growth broad-based? No, 86% from two related parties. Fail.

Is the backlog independent demand? No, mostly one customer, who is also lender and prospective owner. Fail.

Is everything an investor needs disclosed? Yes, it’s all in the S-1. Pass.

One of four. And even the pass carries an asterisk: it’s all disclosed, but only inside a 300-page filing. No deck, no fact sheet, no investor-grade communication around it. Disclosure passes; communication doesn’t.

The price is doing the framing now

Here’s where the three threads tie together and they don’t need me to tie them. Since the first trade, the market has done the reframing the presentation didn’t: it put the operating line, the customer and the counterparty back beside the headline, and repriced. The stock walked from a $386 first-day high back toward the $185 it was sold at. As of early June it was trading in the low-to-mid $200s, a band of roughly $205–$240 since analyst coverage began. At around $220 it’s still up on the offer price and well down from where it closed day one and which of those numbers you quote depends, once again, entirely on what you stand it next to.

That isn’t the market calling Cerebras a bad company. It’s the market doing a CFO’s job in public: pricing in the qualifiers the framing left out.

What the first earnings call will settle

Cerebras hasn’t reported as a public company yet and that call, not the S-1, is where management first frames the story in its own words. Three things to listen for: whether they bridge net income through the operating line themselves; whether they give revenue by customer relationship unprompted; and whether the backlog is presented beside its counterparty. If those show up, the framing was launch-week roughness. If they don’t, it was the strategy. Let’s wait for June 23 when Cerebras ties out their Q1 results.

The Tie-Out

The tie-out is simple. The profit only ties out beside the operating line. The growth only ties out beside the customer base. The backlog only ties out beside the counterparty. Cerebras disclosed those qualifiers; it didn’t frame them. The gap, between a complete filing and clear investor communication, is where the market has stepped in.

The lesson goes beyond Cerebras. Read every headline number beside the thing that gives it meaning: profit beside operations, growth beside concentration, backlog beside counterparty quality. Put the qualifier back in frame, and the story either survives the move or it doesn’t.

With Cerebras, for now, the tape is doing the work.

What’s Next at Tie-Out

AI IPO Tie-Out

✓ SpaceX

✓ Cerebras IPO Review

→ Cerebras Q1 Results: Did the story improve?

→ OpenAI IPO Filing

→ Anthropic IPO Readiness

→ Perplexity’s path to 2028

The CFO Deck Lab

→ Investor deck best practices

→ Award-winning annual reports

→ CFO storytelling frameworks

In Development

→ Annual Report Benchmark Project (US vs Europe)

→ Investor Relations Scorecards

Tie-Out reads below the line. Researched with AI, judged by a CFO.